Residency and Personal Taxation in Cyprus

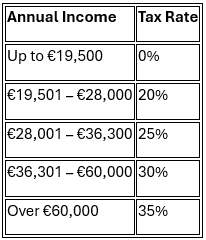

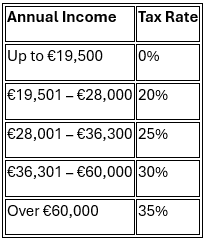

These rates generally apply to income such as:

Employment income;

Business profits;

Professional services income;

Certain crypto-related income depending on classification.

Personal Tax and Cryptocurrency

Under the 2026 reform, gains from the disposal of crypto-assets are taxed at a flat 8% rate regardless of how the activity is classified — occasional investment and frequent active trading are treated identically for disposal gains. Classification remains relevant only for mining rewards, staking income and DeFi yields, which fall outside the disposal gains framework and are subject to general progressive income tax rates (up to ~35%).

Non-Domicile (Non-Dom) Status

In addition to tax residency, Cyprus offers a Non-Domicile regime that provides tax advantages for new residents. Individuals with Non-Dom status may benefit from exemptions from Special Defence Contribution (SDC) on:

Dividend income;

Interest income.

Non-Dom status applies for an initial period and may be extended for two consecutive 5-year periods, subject to conditions under the 2026 reform.

Why Residency Matters for Crypto Investors

Because cryptocurrency transactions are global and digital, tax residency often determines which country has the right to tax crypto-related income. Residency planning can influence:

How crypto gains are taxed;

Reporting and compliance obligations;

Access to favourable tax regimes;

Structuring opportunities through companies.

Careful consideration of residency status is therefore essential before relocating or structuring digital asset activities.

The suitability of this service depends on the individual’s circumstances

Contact us for tailor-made consultation

An individual’s tax residency status in Cyprus plays a central role in determining how their income — including cryptocurrency-related income — may be taxed. Cyprus offers a flexible residency framework and a competitive personal tax system, which has made the country attractive for investors, entrepreneurs, and digital asset professionals. Understanding how residency interacts with personal taxation is essential when assessing potential tax obligations.

Individuals Cyprus residents are taxed at a flat 8% rate on gains arising from disposals of crypto-assets.

Cyprus Tax Residency Rules

An individual may become a Cyprus tax resident under one of two residency tests.

The 183-Day Rule

An individual is considered a Cyprus tax resident if they spend more than 183 days in Cyprus within a calendar year. This is the traditional residency test and is widely used by individuals relocating permanently to Cyprus.

The 60-Day Rule

Cyprus also provides a more flexible 60-day tax residency rule, which may apply if the following conditions are met:

The individual spends at least 60 days in Cyprus during the tax year;

The individual does not spend more than 183 days in any other single country;

The individual is not tax resident in another country;

The individual maintains a permanent residence in Cyprus;

The individual carries out business activities, employment, or holds office in a Cyprus company.

This rule is often used by international entrepreneurs, remote professionals, and investors who maintain international mobility.

Personal Taxation for Cyprus Residents

Individuals who qualify as Cyprus tax residents are generally taxed on their worldwide income, subject to the applicable personal income tax rules. Cyprus applies a progressive personal income tax system, where tax rates increase depending on the level of income. Personal Income Tax Rates (Indicative):

This website provides general information only and does not constitute tax or legal advice. Always seek professional advice tailored to your specific situation. For further information - please contact us and book consultation.

Contact details

Leave your contact details to us

info@cryptocyprus.eu

+357 22 374232

© 2026. All rights reserved.